How much do you need in an ISA to generate a second income of £2,700 a month in 2050?

Image source: Getty Images

No one really knows how much inflation will erode purchasing power by 2050, but what is certain is that the second largest income will still work. And that can be especially true from a tax-free Dividends and Dividends ISA.

Tax exemptions on returns tax the consolidation process. Instead of a small annual leakage of money that would have gone to HMRC, it all stays in the portfolio to grow. And by keeping 100% of those returns, then reinvesting them continuously, the ISA balance snowballs quickly.

Please note that tax treatment depends on the individual circumstances of each client and may change in the future. The content of this article is provided for informational purposes only. It is not intended to be, and does not constitute, any form of tax advice. Students are responsible for conducting their own due diligence and obtaining professional advice before making any investment decisions.

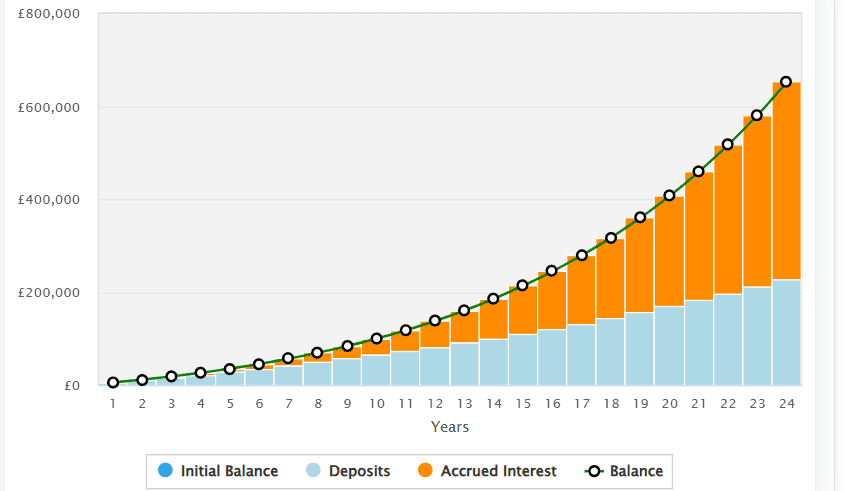

Running calculations

Admittedly, 2050 sounds like a certain year, a time when we will all be driving flying cars and Tesla bots do chores. But it’s actually less than 24 years away, which means we’re closer to 2050 than we were to the start of the millennium in 2000.

To generate £2,700 a month in dividends over that period, a person would invest £425 a month, and compound it by 5% each year. In this case, the ISA would grow to just over £652,000 after 24 years.

This assumes an average 9% annual portfolio return is achieved, with all gains reinvested along the way to truly compound the fuel.

With a portfolio yield of 5%, the income here would be around £32,600 (or the equivalent of just over £2,700 a month).

Obviously these are rough figures, and I didn’t include investment account fees or any trading fees (some platforms still charge for each trade when buying and selling shares).

Also, the 9% return is not guaranteed, although I note that it is much less than FTSE 100Total annual return of about 14.5% over the last five years. And about 10% in the last decade.

Of course, two or three years in a row will quickly reduce those annual returns. The FTSE 100 has been on fire in recent times, but not historically.

Powerful demonstration of wealth creation

These statistics clearly show that investing in a systematic way over time can be really powerful. Even when it starts from scratch.

Meanwhile, contributions, even if they grow by 5% every year, will still be well within the current annual ISA limit of £20,000. I appreciate that not everyone can shell out the full amount.

Investing in UK property

Turning to the dividend stocks of the FTSE 100, I think Londonmetric property (LSE:LMP) is worth considering. This is a real estate investment trust (REIT), with a 10-year track record of rising income.

What I like about this REIT is that it focuses on areas that enjoy strong long-term growth. It has 54% of its portfolio invested in urban transport assets, mainly focused on e-commerce.

Given that we spend more time shopping online, this area has both longevity and growth potential, which should support rising rents.

There is also a focus on health care and convenience, which is clearly pleasing to consistent demand. The senior resident is Ramsay Health Carewhich is a private healthcare provider. The private sector is busy helping the NHS reduce its huge waiting lists.

Of course, if something went wrong at Ramsay, that would be a problem for Londonmetric. High interest rates also pose challenges for REITs because they naturally carry high levels of debt.

As for dividends, however, I like Londometric’s 6% yield. I just added it to my portfolio.