Image source: Getty Images

I FTSE 100 it’s down 1.3% today (March 26), so not many stocks have moved higher. As a result, The next one (LSE:NXT) was the light bulb after it rose 5.2% to 12,665p.

This will bring relief to shareholders, as the stock was down 12% year-to-date before today’s jump. So, what’s exciting the market today?

Unique results

The catalyst for today’s rise was the clothing and home goods retailer’s annual results for the financial year ending January 2026. And as is often the case with Next, it defied doom and gloom for the long-struggling UK retail industry.

Full-year sales rose 10.8% to £7bn, with growth of 7% in the UK and 35% overseas. These figures were significantly higher than the original guidance given almost a year ago (with 5% sales growth).

Meanwhile, pre-tax profit rose 14.5% to £1.16bn, while earnings per share jumped 17%. The business generated £1.1bn in free cash flow, which was exceptional. It returned £839m to shareholders through dividends, share buybacks and other means.

However, although sales in the first eight weeks of this year were promising, management is cautious because of the war in the Middle East. It expects full-year sales to rise 4.5%, with pre-tax profit to rise by the same amount to £1.21bn.

But if the disruption lasts longer than three months, chief executive Simon Wolfson has warned Next will have to raise prices”in the order of 1% to 2%.However, it may be more, depending on the cost increase.

Going forward then, the risk is that consumers tired of inflation will soon tighten their belts, affecting sales growth.

Three considerations

Is Next stock worth considering for long-term investors? Well, I think to answer that, three main factors are considered: the quality of the business, future growth opportunities, and valuation.

In terms of quality, I think Next is top notch. Back in September, I called it “the cream of the crop” among UK retailers, and last year’s results show why.

For example, consider this quote from the report: “Every activity we do – from new warehouses and marketing campaigns to new product launches – must be evaluated in terms of profitability and return on investment. We don’t engage in projects that some might consider ‘strategic’, but offer little hope of high profits or healthy margins..”

It sounds simple, of course. But thanks to world-class handling and execution, The Following actually walks the walk, and delivers the talk. Not many sellers do.

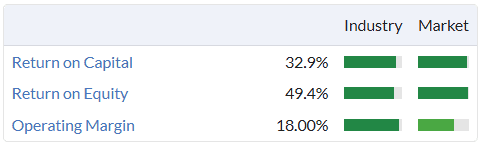

This is reflected in different quality metrics.

In terms of future growth, I think Next has never scratched the surface of a long-term overseas opportunity. International online sales reached £1.3bn last year, a sea level drop in global markets.

For example, it is targeting the expansion of capital-light sales in Asia and the US through online integration platforms. And given the stagnant UK economy, this will be even more important going forward.

What about moderation? Surprisingly, this quality stock is not cheap at nearly 16 times forward earnings (above the 10-year average of 13.5).

But Next has a very strong buyback limit for its shares, and that’s currently £131. With the stock at £126, so I think it’s worth considering, especially for any dips related to the Middle East.

Q2 2026 Earnings Recap")

Gains Attention as a Promising Large-Cap AI Stock")

Q4 2025 Earnings: What Went Wrong")