Rolls-Royce (LSE:RR) has been a stock market darling for over three years now. The stock price chart looks like a plane taking off from the runway, powered by the high-powered Rolls engines.

Today (26 February), the climb continued, once again FTSE 100 the stock is up 6% to around 1,400p after 2025 earnings results.

Here are three key reasons why Rolls-Royce continues to blow away your average stock.

Image source: Getty Images

Targeted fraud is already targeted

Since CEO Tufan Erginbilgiç took over at the beginning of 2023, the change in financial performance has been remarkable.

| FY 2023 | FY 2024 | FY 2025 | |

| Net worth | £15.4bn | £17.85bn | £20.06bn |

| Lower operating profit | £1.59bn | £2.46bn | £3.46bn |

| Lower operating margin | 10.3% | 13.8% | 17.3% |

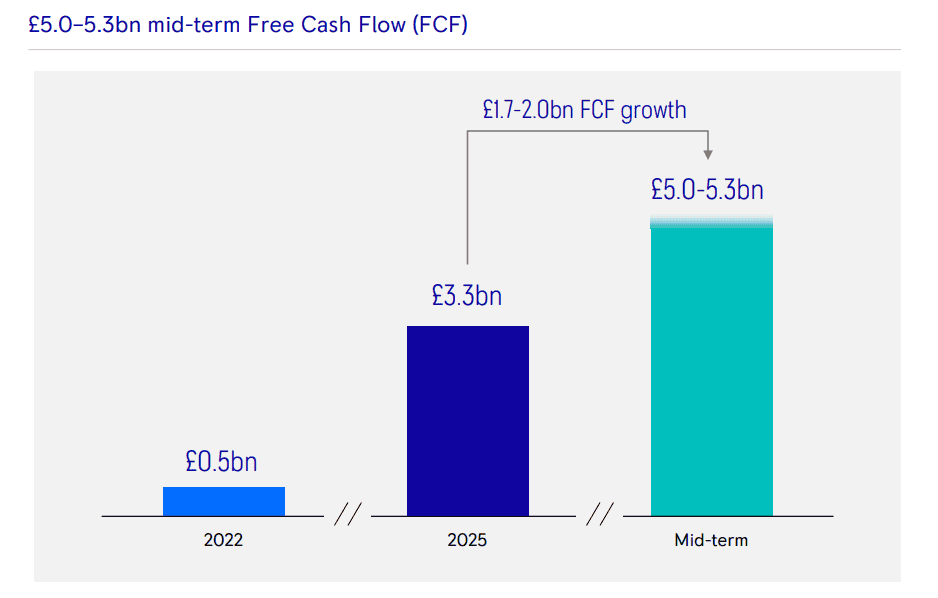

| Free cash flow | £1.28bn | £2.42bn | £3.27bn |

At its stock market day in November 2023, Rolls set a medium-term target (2027) of operating profit of £2.5bn-£2.8bn, with a margin of 13%-15%. It was also targeting free cash flow of £2.8bn-£3.1bn.

This target was considered ambitious at the time. But as we can see above, Rolls-Royce made mincemeat of those by beating them two years it’s early.

It has now raised targets to £4.9bn-£5.2bn in operating profit, 18%-20% in operating margin, and £5bn-£5.3bn in free cash flow. This is expected to be achieved by 2028.

During that time, the restoration of monetary progress has been remarkable. From the original medium-term target of 16%-18%, the new target is 23%-26%.

Erginbilgiç commented: “Our transformation continues with speed and momentum. We always get results that were not possible before our change.” You can say that again.

Needless to say, this kind of outperformance is extremely rare – and the catnip of explosive share price returns.

All categories are firing

Another important thing here is that all three Rolls-Royce divisions are enjoying great momentum.

In Civil Aerospace, where its engines are powerful Airbus 350s and Boeing 787s, renegotiated service agreements, strong demand for travel, and time-on-wing extensions are driving significant growth.

The base operating margin of 20.5% is up from 16.6% in 2024, and engine flight hours should reach 115%-120% of pre-pandemic levels this year.

In defense, there was strong growth in transportation, seaplanes, and helicopters. However, the unexpected star of the show recently has been the Power Systems unit. Here, Rolls is enjoying huge demand from global data center infrastructure to support the AI revolution.

Power generation revenue jumped 30% year-on-year, while the order backlog grew 25% to £6.1bn. This division’s profit increased by 60%!

The magic sauce

Rolls-Royce managed to do what Nvidia couldn’t – engineer a share price drop following the results. The stock’s recovery provided the magic sauce for today’s rise to new highs.

Chris Beauchamp, senior market analyst at IG.

Before today’s release, News of Heaven reported that the engine maker was preparing to announce a share buyback of up to £1.5bn. However, as is the case with Rolls-Royce these days, this too was underrated.

Instead, it will spend a total of £7bn-£9bn on share buybacks from 2026 to 2028, with £2.5bn coming this year. Dividends are back again, although the yield on new money is small.

Now, as exciting as all of this undoubtedly is, it’s worth pointing out the sky-high rating here. The stock trades at 47 times earnings, so any slips in earnings will be punished by the market.

Can Rolls-Royce go even higher? I don’t see why behind these blockbuster results. But I am looking at other, less expensive, UK stocks at the moment.